This method is usually used by small companies where only a few adjusting entries are found at the end of the accounting period. In this method, the adjusting entries are directly incorporated irs says you can amend your taxes electronically, but should you into the unadjusted trial balance to convert it to an adjusted trial balance. The preparation of the statement of cash flows, however, requires a lot of additional information.

Best Wholesale Distribution Software for Small Businesses

After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

Second method – inclusion of adjusting entries directly into unadjusted trail balance:

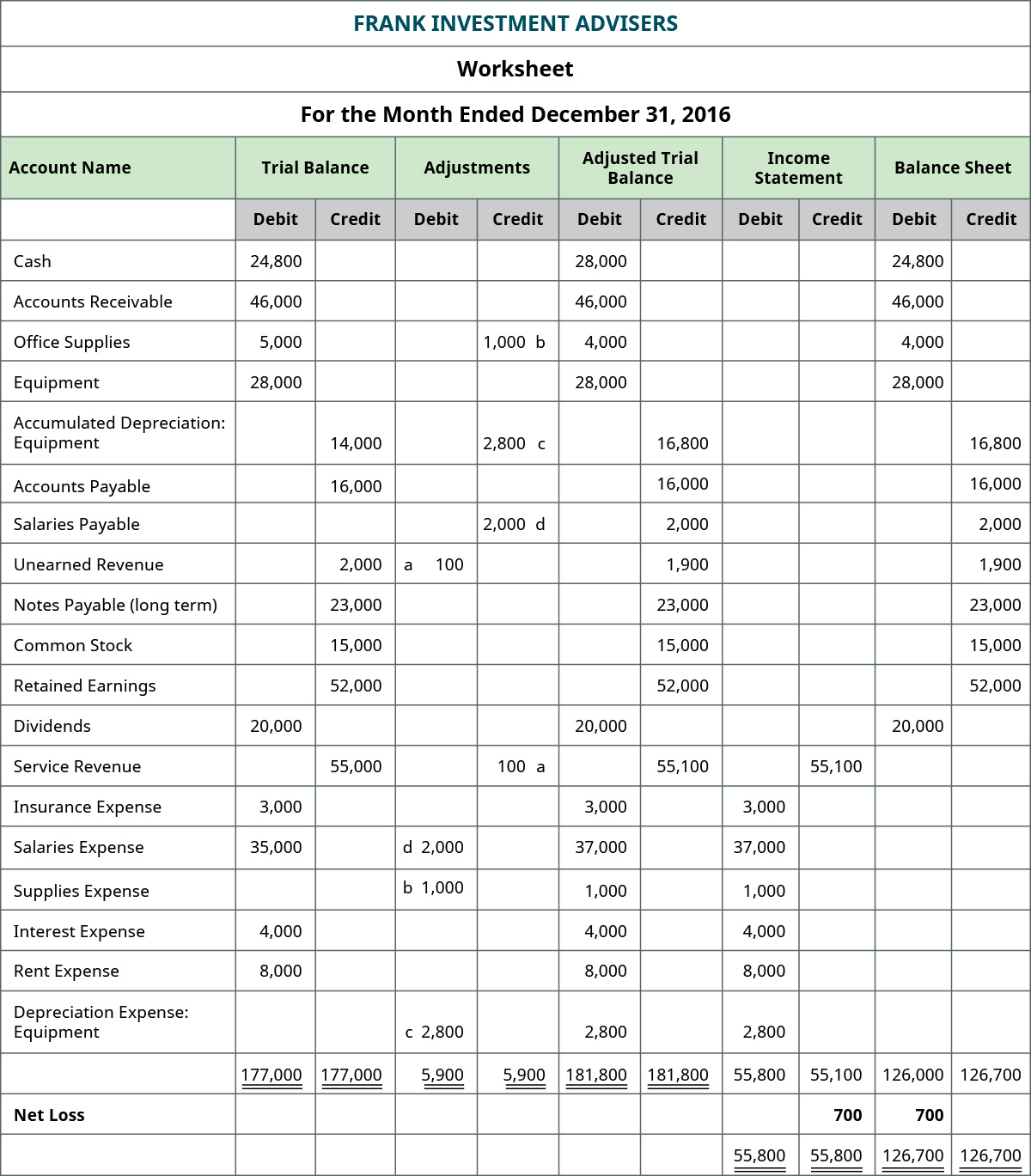

After we post the adjusting entries, it is necessary to check our work and prepare an adjusted trial balance. Understanding how to do this involves preparing an unadjusted trial balance, recording and posting adjusting entries, and ensuring that the final result is accurate. With these skills, you’ll be able to maintain accurate financial records and prepare reliable financial statements for your business. These adjustments are made for items such as accrued revenues, accrued expenses, prepaid expenses, and unearned revenues. Adjusting entries are recorded in the general journal and then posted to the appropriate accounts in the ledger. Such types of transactions are deposits, Closing Stocks, depreciation, etc.

Adjusted Trial Balance Purpose

This adjustment ensures that revenue is recognized in the period it is earned, adhering to the revenue recognition principle. By accurately adjusting unearned revenues, businesses can avoid overstating their liabilities and ensure that their financial statements accurately reflect the income generated from their operations. This process is particularly important for companies that receive advance payments, as it aligns their financial reporting with the actual delivery of goods or services.

- For example, if a company has earned interest income that hasn’t been recorded, you would make an adjusting entry to recognize this income.

- Now that the trial balance is made, it can be posted to the accounting worksheet and the financial statements can be prepared.

- The adjusting entries in the example are for the accrual of $25,000 in salaries that were unpaid as of the end of July, as well as for $50,000 of earned but unbilled sales.

- Before the adjusted TB can be prepared, the year-end adjustments must be made.

This process reduces the book value of the asset on the balance sheet while recognizing the expense on the income statement. By accurately accounting for depreciation, businesses can ensure that their financial statements reflect the true value of their assets and the cost of using them in operations. This adjustment is essential for providing stakeholders with a realistic view of the company’s asset management and long-term financial health. By incorporating adjustments such as accrued revenues, expenses, depreciation, and prepaid expenses, the adjusted trial balance provides a more accurate representation of a company’s financial standing. These adjustments align the accounting records with the accrual basis of accounting, which recognizes revenues and expenses when they are incurred, rather than when cash is exchanged. This approach ensures that financial statements present a realistic view of the company’s operations and financial health.

It is usually used by large companies where a lot of adjusting entries are prepared at the end of each accounting period. The preparation of the adjusted trial balance is the sixth step of the accounting cycle. This trial balance is prepared after taking into account all the adjusting entries prepared in the previous step of the accounting cycle. This initial trial balance includes all the ledger balances before any adjustments are made. List each account and its balance, and ensure that the total debits equal total credits. Adjusted Trial Balance refers to the general ledger balances reflecting adjustments, which include accrued expenditure and non-cash expenses.

This article is not intended to provide tax, legal, or investment advice, and BooksTime does not provide any services in these areas. This material has been prepared for informational purposes only, and should not be relied upon for tax, legal, or investment purposes. BooksTime is not responsible for your compliance or noncompliance with any laws or regulations.

This process enhances the reliability of the financial data and builds trust with stakeholders who rely on accurate information for decision-making. Just like in the unadjusted trial balance, total debits and total credits should be equal. After posting the above entries, the values of some of the items in the unadjusted trial balance will change.